New Report Reveals Why Indian Consumers Are Slow to Adopt Digital Financial Services

MUMBAI, India, May 17, 2017 /PRNewswire/ -- Omidyar Network today released "Currency of Trust: Consumer Behaviors and Attitudes Toward Digital Financial Services in India," a research report that brings the voice of the consumer to the forefront of the discussion around adoption and usage of digital financial services in India. The report focuses on understanding the current context and behaviors of a diverse sample of Indian consumers regarding their digital consumption and readiness for digital financial services on key issues, such as ease of use, trust, and social collaboration. It also offers providers a practical set of recommendations to better reach financially underserved consumers in the country with digital financial offerings.

"India has made tremendous progress in building infrastructure and regulatory frameworks that encourage digital innovation in financial services, but adoption and usage of new offerings have been slow to take hold and scale," said Tilman Ehrbeck, partner at Omidyar Network. "We believe that a deeper understanding of consumers' behaviors and aspirations is at the crux of unlocking higher usage and providing services that are more relevant to consumers' real needs."

The report findings come as a result of in-depth interviews and human-centered design prototyping sessions with consumers across 30 communities in Nagaland, Bihar, Maharashtra, Karnataka, and Telangana, covering a mix of rural, semi-urban, and urban areas. Among the most relevant behavioral insights surfaced by these deep interactions with Indian consumers are:

- Even though smartphone adoption is expected to reach a projected 54 percent of the Indian market in the next three years, a large portion of surveyed consumers—especially those in rural areas—indicated they are comfortable with keeping their basic feature phones. This is primarily due to the greater resilience and longer battery life of lower-end phones, but also because internet access is not seen as a priority for these consumers. This means digital financial services providers will need to cater to both technologies in their offerings in order to broaden their customer base.

- Adoption of mobile apps is driven by data efficiency and usage within consumers' social networks. The survey found that Indian consumers are frugal when it comes to data usage and look for creative ways to save data, such as constantly alternating between 2G and 3G depending on the function in use or pooling resources to set up shared Wi-Fi hot spots. Consumer adoption is also influenced by the number of individuals in their social network who use the same app. This means digital financial services apps need to be lean in data usage and leverage pervasive platforms, such as Whatsapp or UCBrowser.

- Consumers are willing to leapfrog traditional financial services and adopt digital if they find convenience, relevance, and alignment with socio-cultural norms. Despite the low comfort level and lack of familiarity with digital financial services, through prototyping sessions, many surveyed consumers expressed a willingness to start using such apps if the technology addresses unmet needs, offers convenience, and doesn't challenge socio-cultural norms. To shift consumers from existing informal cash–based financial solutions to formal digital financial products, solutions need to capture their full relationship and experience with money, such as allowing consumers to create partitions or "virtual jars" within an account, and offer them tools that can help with cash flow management of micro- and small businesses or household expenditures.

- Current digital financial offerings are seen as overly complex even by savvy consumers. Surveyed consumers consider those who use financial service apps to have a specialized skill and cite difficulty grasping financial jargon in on product offerings and legal terms and conditions. According to the research, consumers' lack of trust in their own abilities is one of the biggest hurdles today for adoption of digital financial services. Lowering the stakes for consumers to experiment with digital offerings is a must for providers. Prototyping sessions revealed that simple actions such as removing jargon and complex user interfaces, communicating in local languages, offering easy proof of transaction and grievance redressal, and using bank correspondents to onboard customers, can go a long way in building consumers' confidence to transact digitally.

"Trust has always been the cornerstone of the banking and financial services industry," said Smita Aggarwal, investments director at Omidyar Network. "But what we have learned from consumers in the field is that providers tend to prioritize time and resources in building trust in their brand, when trust in product reliability and users' self-trust are the ones that really move the adoption needle."

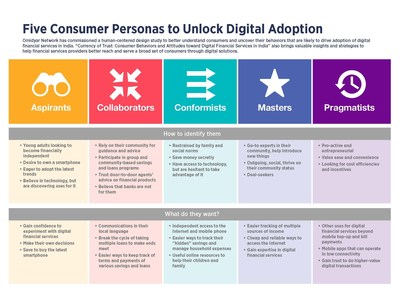

A deep analysis of the consumer data collected also revealed that adoption of digital financial services is influenced mainly by individual personality traits, socioeconomic status, and access to technology. These characteristics allowed the grouping of consumers within category profiles with shared attributes, attitudes, behaviors, needs, socioeconomic, and demographic status, which we have called "personas."

| Persona |

How to identify them? |

What do they want? |

|

Aspirants |

• Urban or semi-urban men and women between the ages of 15-30 years who own a basic feature phone, but aim to upgrade to a smartphone • Young adults looking to become financially independent • Eager to adopt the latest trends • Believe in technology, but are still discovering uses for it

|

• Gain confidence to experiment with digital financial services • Make their own decisions • Save to buy the latest smartphone |

|

Collaborators |

• People between the ages of 25 and 50 who live in semi-urban or rural areas. Men in this group own a basic phone or a "dark smartphone" (with no internet access), while women do not typically own a phone • Rely on their community for guidance and advice • Participate in group and community-based savings and loans programs • Trust door-to-door agents' advice on financial products • Believe that banks are not for them

|

• Communications in their own language • Break the cycle of taking multiple loans to make ends meet • Easier ways to keep track of terms and payments of various savings and loans |

|

Conformists |

• Women between the ages of 20-50 in semi-urban or urban areas who own a smartphone • Restrained by family and social norms • Save money secretly • Have access to technology, but are hesitant to take advantage of it

|

• Independent access to the internet and mobile phone • Easier ways to track their "hidden" savings and manage household expenses • Useful online resources to help their children and family

|

|

Masters |

• Female Masters tend to be between 25 and 50 years of age, live in semi-urban or rural areas, and own a basic feature phone, while male Masters tend to be between 15 and 35 years, live in urban areas, and own a smartphone • Go-to experts in their community, help introduce new things • Outgoing, social, thrive on their community status • Deal-seekers

|

• Easier tracking of multiple sources of income • Cheaper and more reliable ways to access the internet • Gain expertise in digital financial services

|

|

Pragmatists |

• Men between the ages of 25-50 who own a smartphone with data services • Proactive and entrepreneurial • Value ease and convenience • Looking for cost efficiencies and incentives

|

• Other uses for digital financial services beyond mobile top-up and bill payments • Mobile apps that can operate in low connectivity • Gain trust to do higher-value digital transactions

|

As summarized in the table above, each persona type requires a different pathway through which providers can initiate or increase engagement with their digital financial services, thereby offering a valuable framework to unlock customer acquisition and help scale digital financial services in India.

The full report can be downloaded at: www.omidyar.com/insights/currency-trust

An infographic on the five consumer personas can be downloaded at: www.omidyar.com/spotlight/currency-trust

About Omidyar Network

Omidyar Network is a philanthropic investment firm dedicated to harnessing the power of markets to create opportunity for people to improve their lives. Established in 2004 by eBay founder Pierre Omidyar and his wife Pam, the organization invests in and helps scale innovative organizations to catalyze economic and social change. Omidyar Network has committed more than $1 billion to for-profit companies and nonprofit organizations that foster economic advancement and encourage individual participation across multiple initiatives, including Education, Emerging Tech, Financial Inclusion, Governance & Citizen Engagement, and Property Rights. To learn more, visit www.omidyar.com, and follow on Twitter @omidyarnetwork #PositiveReturns.

Issuing Organization:

Omidyar Network

Photo - http://mma.prnewswire.com/media/512655/Omidyar_Network_Five_Consumer_Personas_Infographic.jpg

Photo - http://mma.prnewswire.com/media/512653/Omidyar_Network_Journey_to_Reach_Consumers_Infographic.jpg

Share this article